NFourSID¶

Overview¶

Implementation of the N4SID algorithm for subspace identification [1], together with Kalman filtering and state-space models.

State-space models are versatile models for representing multi-dimensional timeseries. As an example, the ARMAX(p, q, r)-models - AutoRegressive MovingAverage with eXogenous input - are included in the representation of state-space models. By extension, ARMA-, AR- and MA-models can be described, too. The numerical implementations are based on [2].

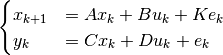

The state-space model of interest has the following form:

where

is the timestep,

is the timestep, is the output vector with dimension

is the output vector with dimension  ,

, is the input vector with dimension

is the input vector with dimension  ,

, is the internal state vector with dimension

is the internal state vector with dimension  ,

, is the noise vector with dimension ,

is the noise vector with dimension , are system matrices describing time dynamics and input-output coupling,

are system matrices describing time dynamics and input-output coupling, is a system matrix describing noise relationships.

is a system matrix describing noise relationships.

Code example¶

An example Jupyter notebook is provided here.

References¶

Van Overschee, Peter, and Bart De Moor. “N4SID: Subspace algorithms for the identification of combined deterministic-stochastic systems.” Automatica 30.1 (1994): 75-93.

Verhaegen, Michel, and Vincent Verdult. Filtering and system identification: a least squares approach. Cambridge university press, 2007.